Exploring Low Holder Counts and Lack of DeFi Utility in Treasury RWAs

$BENJI, $BUIDL, $VBILL and $TBILL have less than 15 combined holders and no DeFi integrations - Why?

- Published:

- Edited:

To the average DeFi user, tokenized stocks make perfect sense. A trusted custodian holds the “real” stocks and manages mints and burns, and network participants have free rein to use onchain stocks however they see fit.

On the other hand, tokenized U.S. Debt Treasuries, like Franklin Templeton’s $BENJI, BlackRock’s $BUIDL, and VanEck’s $VBILL, are a bit harder to grasp for DeFi power users.

Like tokenized stocks, one look at SolScan confirms these assets are verifiably onchain. However, unlike tokenized stocks, many U.S. Treasury Assets cannot be traded, collateralized, lent out, or borrowed in the DeFi economy.

This begs the question: Why bother? Why put these time-tested assets onchain if they can’t take advantage of any of the benefits of being on a permissionless system?

Why do U.S. treasury assets need to be treated differently, and how is bringing them onchain mutually beneficial for both Solana users and institutional funds?

The Concerns Surrounding Onchain U.S. Treasuries

Discussing onchain U.S. Treasuries is shaky ground, largely because the term applies to a large umbrella of applicable assets. RWA.xyz, perhaps the industry’s leading resource for RWA data, separates U.S. Treasury assets from traditional stablecoins, and rightly so, while still considering “stablecoins” with yield-bearing properties, like Ondo’s $USDY, as tokenized treasuries.

However, while $USDY and similar assets like OnRe’s $ONyc are publicly tradable on decentralized exchanges and widely integrated in Solana DeFi, other treasury assets live in walled gardens. This is due to a wrath of regulatory constraints, but more on that later.

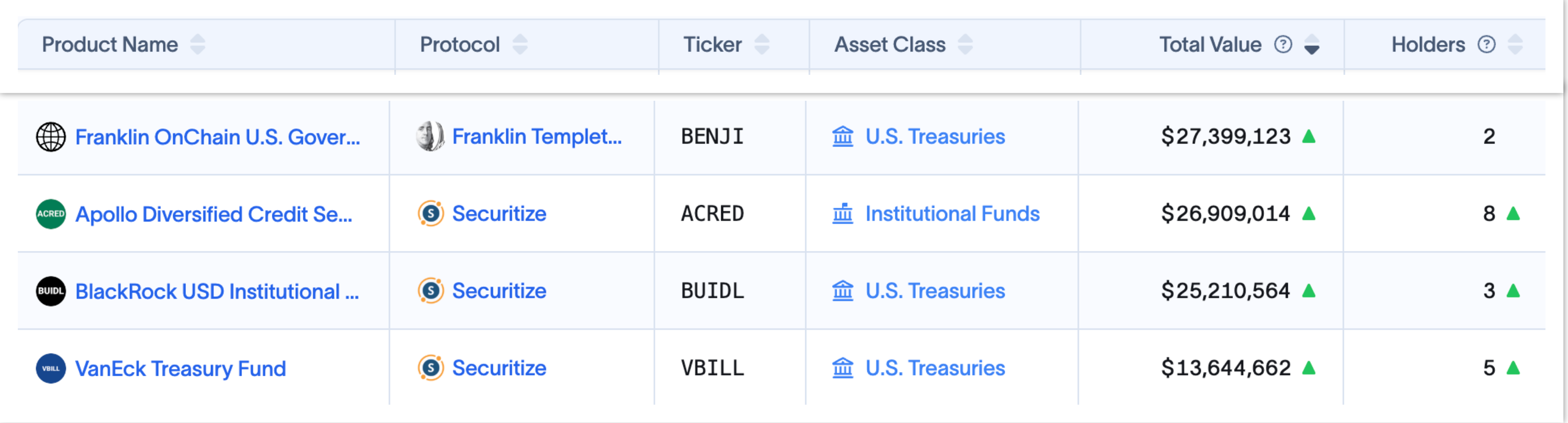

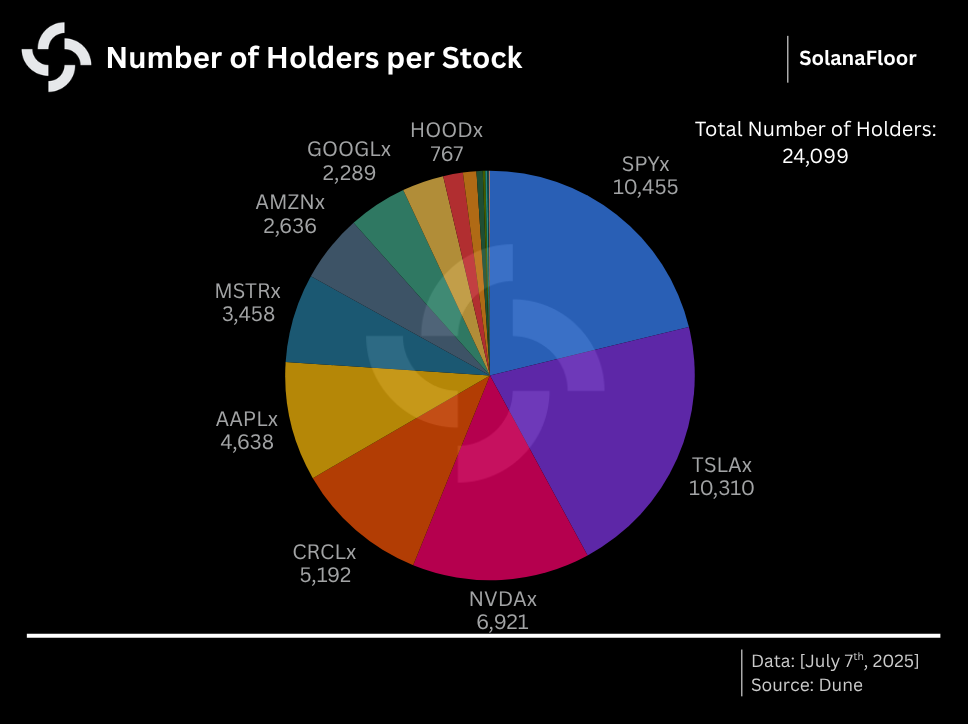

The likes of $BENJI, $BUIDL, and $VBILL have enjoyed steadily growing market capitalizations in recent months, but their holder counts remain questionably low.

On paper, tokenized treasury assets appear to have remarkably low onchain adoption rates. This suggests one of two things: Either nobody wants exposure to these assets, or access to “onchain” tokens isn’t as democratic as we’ve been led to believe.

Solana’s tokenized stocks have amassed over 24,000 holders in a matter of days, indicating that DeFi users are overwhelmingly eager to get their hands on RWAs.

If it were as simple as buying these tokens through Raydium, surely hundreds more people would want tokenized US treasury exposure.

What’s more likely is that issuers maintain centralized control and custody over these assets. One possible explanation is that tokens are minted and held in a small number of secure wallets on behalf of investors, who can track their contributions to the funds via specific applications, like Franklin Templeton’s BENJI app. SolanaFloor repeatedly engaged Franklin Templeton for clarity on the matter, but the asset manager has in so far declined to comment.

A statement from a Securitize representative outlined the issuance mechanics of tokenized treasury assets:

“Funds like BUIDL or vBILL on Solana are native, meaning the fund itself is tokenized and subscription/redemption processes happen with the fund. Investors invest in fiat or stablecoins and the fund deploys that capital as described in the offering documents and mints a token. With respect to redemption the fund liquidates assets or uses reserve liquidity to burn/redeem the token of the investor for cash or stablecoins, as applicable. In certain cases the fund itself can hold digital assets (like stables) making atomic subscription possible.” - Unnamed Securitize Spokesperson.

While this undoubtedly adds a substantial layer of “trust me bro” to tokenized treasuries, TradFi giants like Franklin Templeton are trusted household names for a reason. Holders may not have self-custodial control over their tokens, but this demographic of investor likely doesn’t care about these nuances.

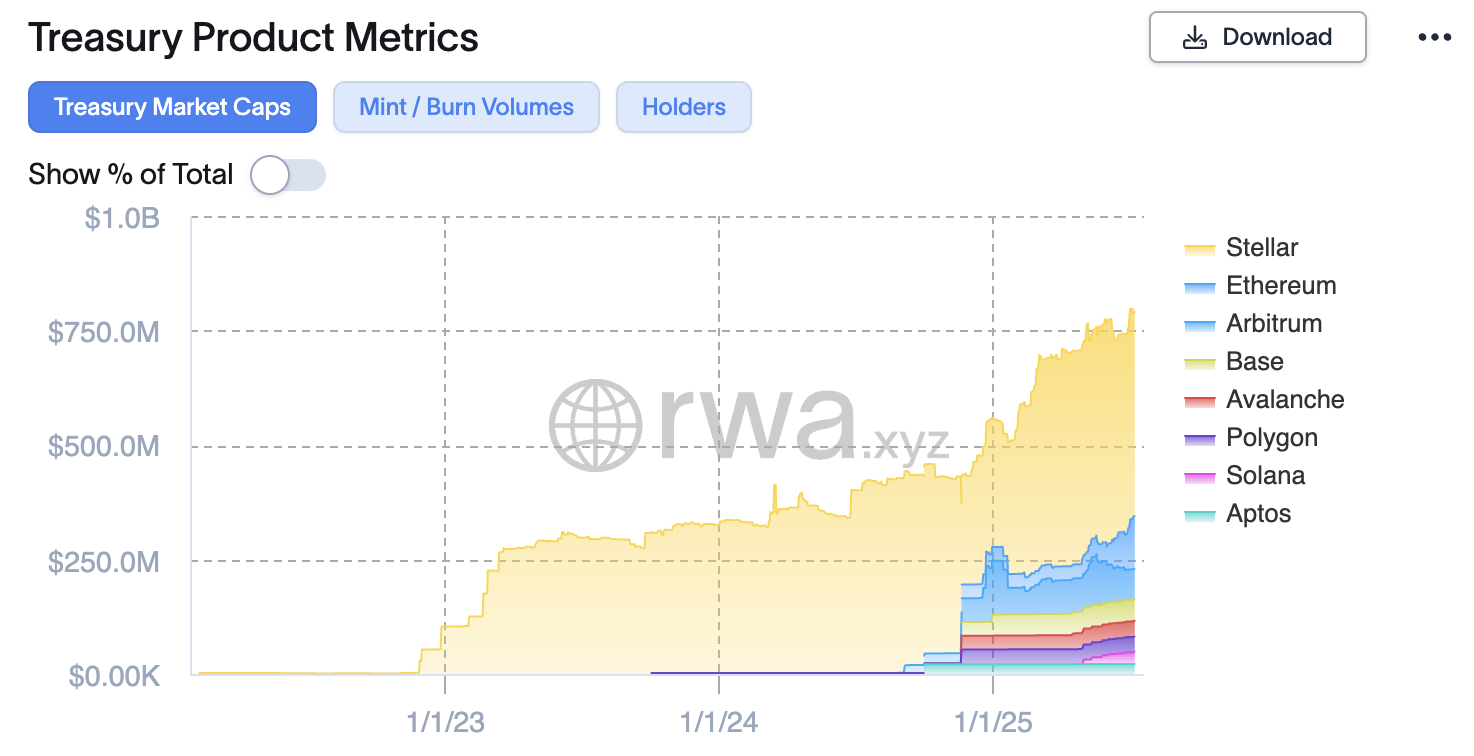

Taking a wider, multi-chain view of tokenized treasuries, Solana is still far behind rival chains. Based on RWA.xyz data, the total market cap of Solana-based treasury assets constitutes a mere 5.6% of Ethereum’s, and even trails far smaller networks like Stellar.

For all Franklin Templeton’s optimism toward Solana, as evidenced by spot ETF filings and a wealth of supportive research reports, $BENJI has proven far more popular among Stellar users.

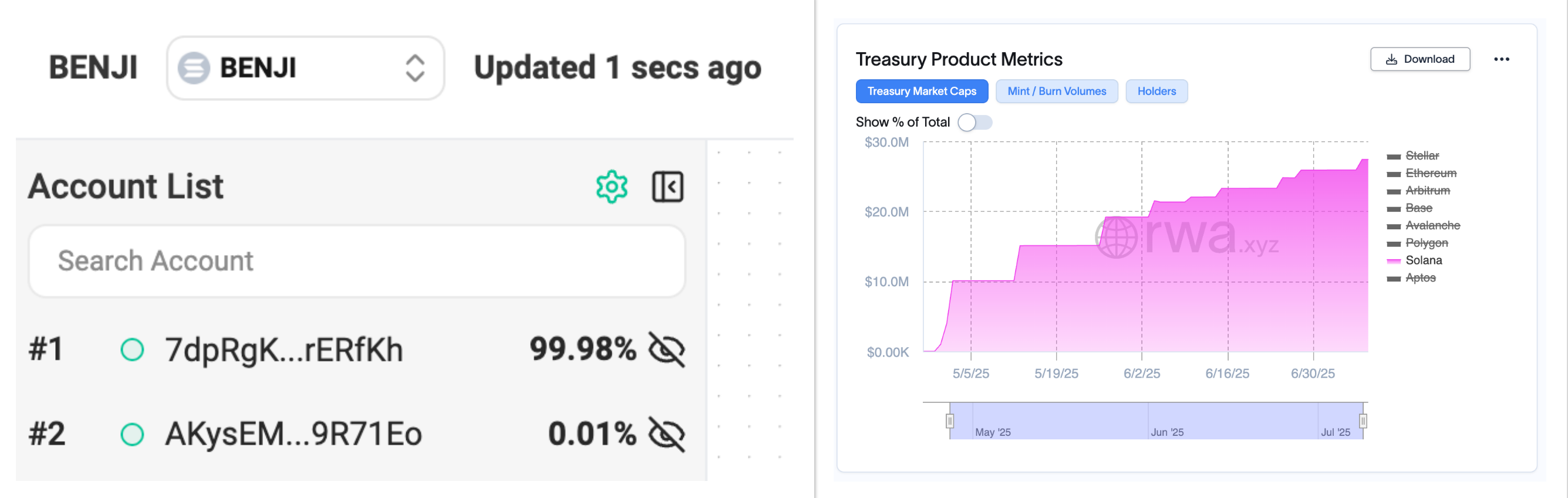

The market cap of Stellar-based $BENJI is over 1,500% higher than on Solana, with 639 holders compared to Solana’s 2. Despite one wallet holding over 99.98% of Solana’s circulating $BENJI, the fund’s market cap has steadily increased from $10M to $27M.

This suggests that either Franklin Templeton manages token custody on behalf of its users, or that the fund only has two investors.

RWA.xyz Head of Research Bryan Choe argues that Solana is reclaiming lost ground after a slow start in the RWA arms race. Choe suggests that certain funds, like Apollo’s $ACRED, is outperforming on Solana, while insinuating that Stellar’s supposedly outsize success in the RWA sector is due almost entirely to $BENJI alone.

“Tokenized assets have historically received less spotlight within the Solana ecosystem and the RWA ecosystem has developed at a slower pace. That said, RWAs are certainly getting a lot of attention on Solana, and TradFi issuers like Apollo are very interested in exploring the ecosystem. ACRED (Apollo's tokenized credit fund) has more market cap on Solana vs. Ethereum… Aside from Ethereum, Stellar does lead the pack at ~$460M of market cap. But if you take a deeper look, BENJI accounts for 98% of its market cap. Stellar was the first chain that BENJI was launched on, so it has a different strategic/historical background. While the high-level metrics paint the picture certain way, I don't think it's accurate to say Stellar has enjoyed extraordinary success with RWAs. Rather, it's more that Stellar has enjoyed success with $BENJI.” - Bryan Choe, RWA.xyz Head of Research

Why U.S. Treasuries Need to be Treated Differently

Tokenized stocks, like those soon to be provided by Remora Markets, have made it possible for anyone, anywhere in the world, to trade the world’s biggest companies, 24/7. Tokenized U.S. treasury assets do not promise the same accessibility. As mentioned, this is primarily due to regulatory restrictions.

Funds like BUIDL and BENJI operate under far stricter regulations enforced by U.S. securities laws and are limited to accredited investors who pass KYC and anti-AML procedures. Most tokenized treasury assets are additionally subject to transfer restrictions, meaning they can only interact with whitelisted wallets.

Our previously mentioned Securitize representative stipulated that DeFi protocols typically assume that onchain tokens are bearer instruments, meaning that ownership of the asset resides with the holder. Given that this is not case for the securities in question, like $BUIDL and $BENJI, DeFi is ill-equipped to service these assets.

“DeFi protocols generally presuppose bearer instruments, but RWAs that are securities are not bearer instruments and require specific regulations that create hurdles when ownership cannot be matched to individuals/entities… Furthermore, securities often have transfer restrictions and other legal requirements that DeFi protocols may not be able to support.” - Unnamed Securitize Spokesperson

At first glance, surpassing the composability barrier looks like a legislative dead end. But the crypto industry hasn’t been called the cutting edge of innovation erroneously. Securitize is actively working on solutions that empower investors to get maximum utility out of these assets, namely through their proprietary sToken model.

“We have and continue to develop ways to utilize our tokenized securities in DeFi protocols and provide other composability, such as the ability to pledge as collateral on crypto exchanges… From a technical perspective, sTokens are SPL tokens and not a new standard. Their advantage is they represent an unencumbered position in a certain RWA but are not the RWA itself, which allows them to operate in DeFi with less friction than the direct usage of RWA.” - Securitize

$sACRED, Securitize’s pioneering sToken offering a more DeFi-ready representation of Apollo’s yield-bearing ACRED fund, has found a home in Kamino’s lending market.

While $sACRED cannot be freely traded on a decentralized exchange, accredited holders can borrow stablecoins against their holdings.

The Perks of Tokenized Treasury Assets

Courtesy of progress and ongoing development from teams like Securitize, tokenized treasury assets are steadily finding wider utility within an expansive DeFi ecosystem.

But there has to be more to it. The world’s biggest financial institutions likely wouldn’t have been willing to cowboy millions of dollars in treasury assets onto a public blockchain so that a select few accredited investors can borrow $USDC.

Solana Foundation Head of Institutional Growth Nick Ducoff highlights some additional benefits, citing programmatic yield and greater asset transfer flexibility as key differentiators to offchain equivalent assets.

“Asset managers like Franklin Templeton are making incredibly important contributions by moving the RWA conversation forward with regulators and have innovated within the constraints they have. For example, Franklin Templeton allows peer-to-peer transfer of BENJI among whitelisted wallets. Tell me how you would send shares of fund XYZ in your brokerage to someone else? You couldn't really do it. So they are innovating. Also, they take a snapshot for interest payments every block, so if you hold their money fund for part of the day, you get that part of the day's interest. That isn't the case with traditional money funds.” - Nick Ducoff, Solana Foundation Head of Institutional Growth

Ducoff asserts that TradFi issuers are committed to innovating further and bringing legacy financial constructs up to speed in an onchain economy, despite the regulatory limitations. If the SEC continues to modernize its regulatory framework, the industry may benefit from fewer compliance hurdles in the years to come.

U.S. Treasuries and the DeFi Crowd

Where does this all leave us today? Solana-based treasury assets are steadily gaining traction amongst accredited investors, despite their lack of composability when compared to traditional DeFi assets.

While there may be some lingering concerns around the custody practices, the reality is that these assets are not designed for DeFi purists. As such, tokenized treasury assets may struggle to find meaningful adoption in an open onchain economy.

That being said, institutional operators and accredited investors may find assets like $BUIDL and $BENJI preferable to offchain alternatives. Flexible asset transfer between whitelisted wallets is a niche unlock for these players, and the prospect of programmatic yield accrual could mean that holders’ wealth compounds faster.

If anything, the user disparity of demand between the two sectors is indicative of crypto’s wider maturation. Horizontal demographic scaling and institutional inflows are undoubtedly a net positive for Solana.

Different types of products are useful to different types of people for different reasons, and that’s okay.

Read More on SolanaFloor

$PUMP tokenomics revealed ahead of ICO

Pump.fun Confirms $1.3B ICO - Allocates 24% of Supply to Community Incentives

Explore Intermediate DeFi Strategies on Solana