Centralized Systems Are Failing: Who is at risk?

The financial world has recently witnessed a number of banking events that could potentially impact a wide range of customers. This article aims to provide an overview of the recent news surrounding banks and analyze who is most at risk.

- Published:

- Edited:

The financial world has recently witnessed a number of banking events that could potentially impact a wide range of customers. These events have sparked debates among experts and raised concerns about the stability of the banking industry. This article aims to provide an overview of the recent news surrounding banks and analyze who is most at risk.

Increase in Cybersecurity Threats

Recent months have seen a significant rise in cyberattacks targeting banks and financial institutions. These attacks have ranged from data breaches to ransomware, exposing sensitive customer information and causing financial losses. While banks have taken measures to strengthen their cybersecurity infrastructure, the evolving nature of cyber threats poses a challenge.

In fact, one of the largest bank heists in the world occurred in February 2016, and it was not a physical robbery. The Bangladesh Bank Robbery was an attack on the bank itself, using the SWIFT credentials to send more than 35 money transfers that were fraudulent.

By requesting the Federal Reserve Bank of New York to transfer millions from the Bangladesh Bank to bank accounts in the Philippines, hackers were able to steal $101 million in 4 of the many requests. Why didn't the rest of the transactions go through? The hackers withdrawing wanted money to be sent to the Shalika Foundation, but ended up writing it as "Fandation," raising alarms at the Federal Reserve bank. If not for the typo, up to $1 billion could have been stolen from the bank's own accounts.

At-risk customers: Primarily, high-net-worth individuals and large corporations are at risk, as they are often the prime targets for cybercriminals. However, all banking customers should be vigilant and take necessary precautions to protect their accounts and personal information.

Rising Interest Rates

Persistently rising interest rates have pressured banks' profitability, as many institutions put billions in mortgage-back securities and low yield bonds. As a result, companies like Silicon Valley Bank ended up going bankrupt. Through poor risk management and not hedging for rising interest rates, SVB and other banks ended up losing billions.

Initially, SVB's financial position was impacted by the decrease in resale price of US treasuries, which comprised the majority of its invested funds due to rising interest rates. This reduction in value alone did not cause SVB to go bankrupt, as long as they did not have to sell the older bonds they held at a reduced price.

However, a subsequent blow forced SVB to sell these bonds at a significant discount, leading to financial problems. This was due to inflation causing the Fed to cease quantitative easing, stopping the flow of funds that were supporting the soaring stock prices of Big Tech companies like Google, Amazon, Meta, Twitter, Netflix, Airbnb, and Uber.

These companies had used loans secured by overvalued stock prices as collateral, and the sudden depletion of funds caused them to withdraw deposits from banks such as SVB. This further contributed to the financial issues faced by SVB.

At-risk customers: Savers and those relying on banks to manage their funds may be adversely affected by rising interest rates, including SVB depositors and depositors around the world in other institutions that may face after effects.

Regulatory Changes

In response to economic developments, regulatory bodies worldwide have been updating banking rules and policies. These changes often aim to strengthen the financial system and protect consumers, but can also create uncertainty and additional costs for banks.

At-risk customers: Small and medium-sized businesses, as well as individual customers, may find it more difficult to access banking services as a result of these regulatory changes. Banks might impose stricter lending requirements, making securing loans or credit harder for these customers.

Bank Mergers and Acquisitions

The competitive landscape of the banking industry has led to a wave of mergers and acquisitions, as banks aim to achieve economies of scale, streamline operations, and expand their customer base. While this consolidation may provide benefits for the banks involved, customers may face disruptions or reduced options.

At-risk customers: Customers of merging banks may experience changes in fees, account terms, or customer service quality. Small businesses and local communities may be particularly affected if the consolidation leads to branch closures or reduced access to banking services.

Conclusion

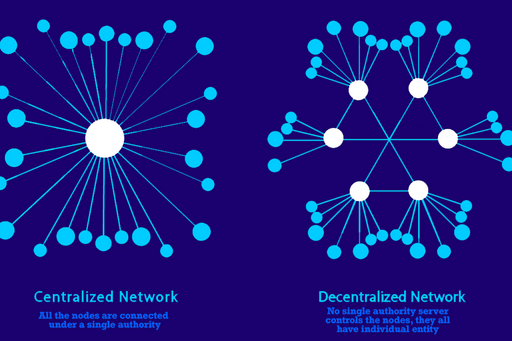

With centralized banking opportunities, these concerns all pose a real threat to the stability of trusted banking. However, in crypto, the trustless and decentralized nature of financial instruments on-chain provides a much safer alternative. There are no centralized points of failure where someone can fraudulently access your wallet to sign transactions and drain your funds, no government-decided inflation or monetary policies that are obscure and designed for control, and definitely no limitations to access financial instruments, such as loans or investing. With the impending fall of traditionally centralized finance, decentralized finance stands the most to gain; and will make the world a better place.